Finance

What we can learn from Singapore Government’s budgets for the last 7 years

By Valuepenguin.sg

The government of Singapore is set to announce its budget plans for 2017 on Monday, 20 Feb 2017. While media is already buzzing about what we could expect to hear from Minister Heng Sweet Keat next week, few have covered what actually has been happening with the government spending for the last few years. Often, we can glean valuable insights for the future by looking back into the past. Here, we attempt to distill a few major trends we observed about the government’s budget since 2010, and assess what it could possible mean for what’s in store for the next few years.

Government Revenue Is Becoming More Dependent On Consumers, Not Companies

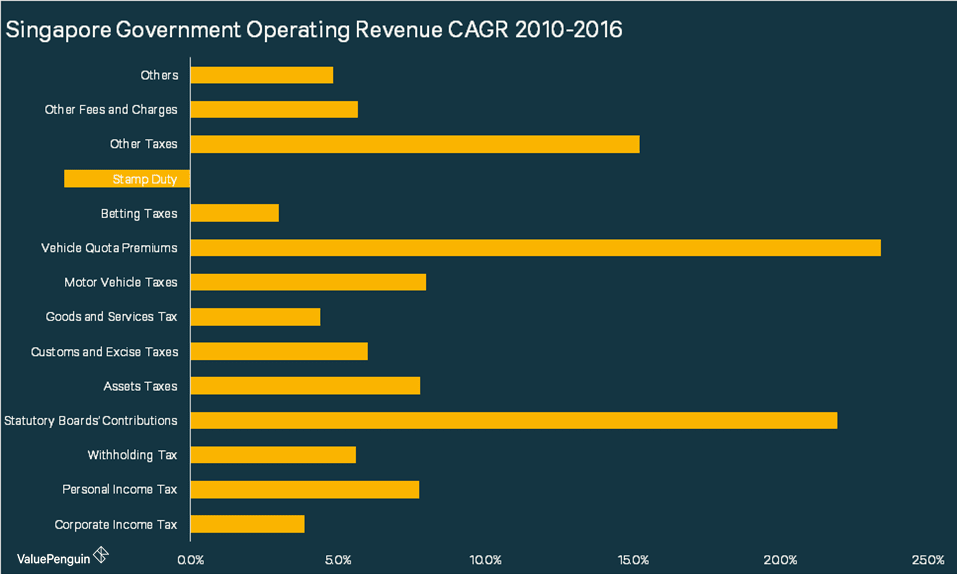

The Singapore government’s budget has been becoming more reliant on taxes on consumers rather than on companies. From 2010 to 2016, the government’s operating revenue has increased by about 6.8% per year from S$46bn to S$68bn, while various taxes on consumers have grown at a faster pace. For instance, personal income tax has grown at 7.8% per year, motor vehicle taxes and vehicle quota premiums have grown at 16.5% per year, and other taxes (including water conservation tax, foreign worker levy, development charge and annual tonnage tax) have grown at 15.2% per year. In the meantime, corporate income tax has grown at a slower pace of 3.9% per year.

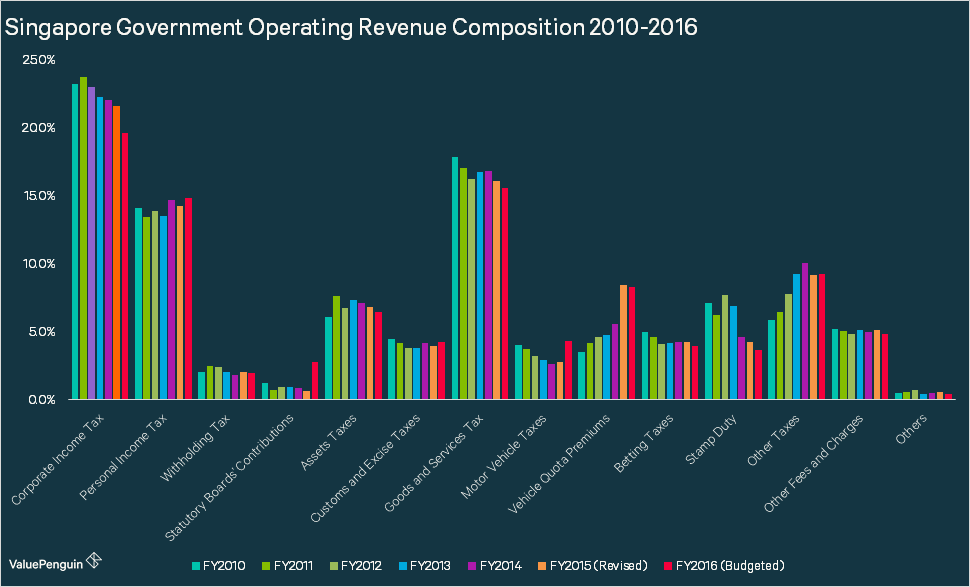

This implies that corporate income tax has gone from being 23% of government revenue in 2010 to 20% in 2016, while the aforementioned 3 categories have gone from 27.4% of government revenue in 2010 to 36.6% in 2017. This may be a result of the government’s attempt to help businesses stay profitable or operational in face of stagnating economy. Such a move may have helped in reducing unemployment by keeping more companies afloat, meaning that the unemployment rate that has been rising recently could have been higher otherwise.

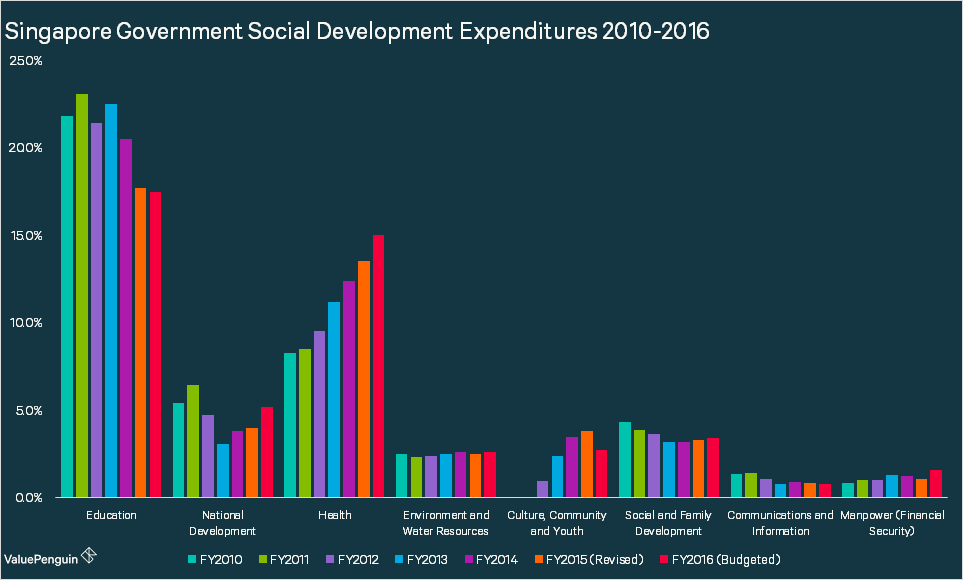

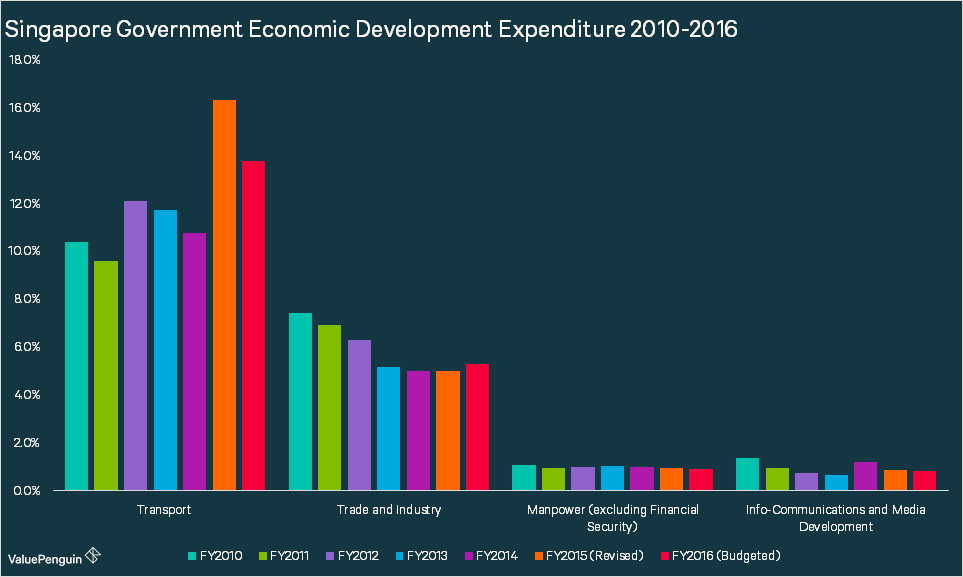

Government Expenditure Increasingly Focused on Development & Social Safety, but Not Education & Technology

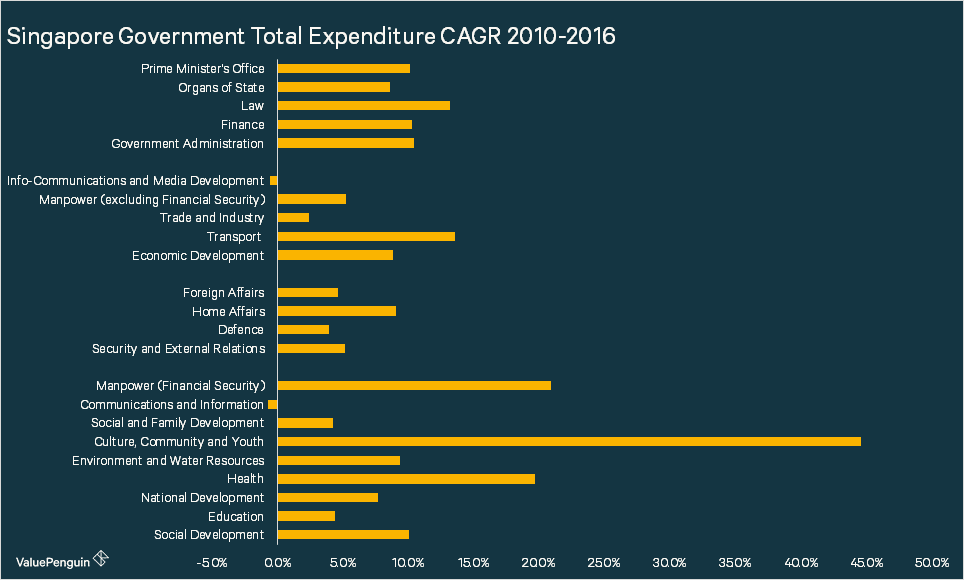

Overall, the Singaporean government’s expenditure has increased by about 8.4% per year since 2010 to 2016 from S$45bn to S$73bn, slightly faster than its revenue growth rate of 6.8%. The main drivers of this growth has been social development (10.1% per year) and health development (19.7% per year).

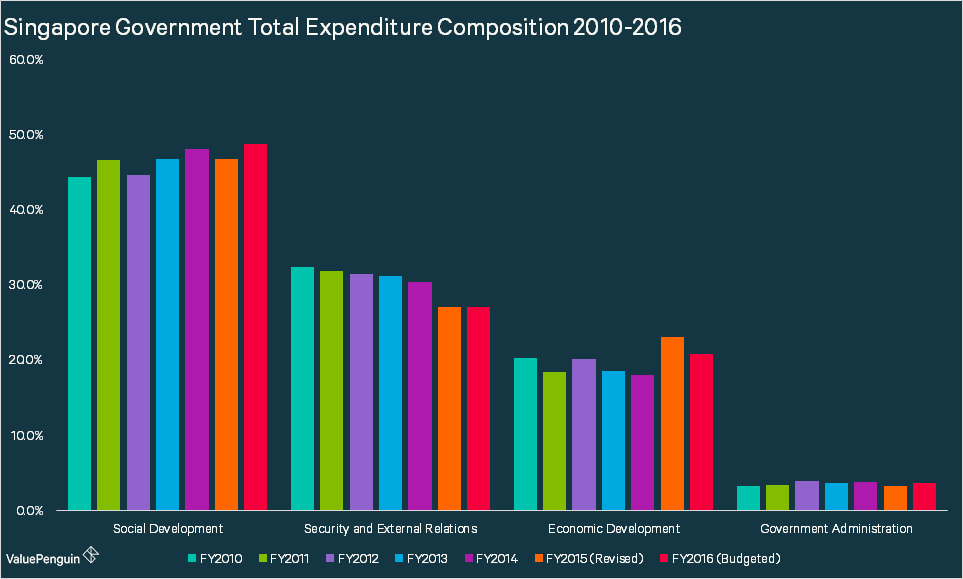

Essentially, the government has been shifting money away from security & external relations in order to invest in its social and economic infrastructures since 2010. For instance, security and external relations represented 32.3% of government’s budget in 2010. By 2016, this portion had declined to 27%. This decline was almost entirely offset by social development, whose proportion increased from 44.3% in 2010 to 48.7% in 2016.

What’s particularly interesting about this growth in social development expenditure is how the government has increased its spending massively for health from 8.3% in 2010 of budget to 15% of budget in 2016. This reflects the ageing population in Singapore, and the government’s conscious effort to provide necessary care for the elderly. However, the government has also decreased the portion of its budget going into education, which grew by only 4.4% per year and represents 17.4% of its budget in 2016 compared to 21.8% in 2010.

The government of Singapore continues to invest in its infrastructure to create jobs. From 2010 to 2016, economic development expenditure grew by 8.9% per year, of which investment in transport grew at the quickest pace at 13.6% per year. Transport was the 4th biggest spending area for the government in 2016, representing about 13.8% of total budget in 2016 compared to 10.4% in 2010. In contrast, economic development expense in info-communications and media development actually declined by -0.6% per year.

What Could We Expect from 2017?

While our team at ValuePenguin tend to stay away from making bold predictions without substantial data and evidence, there are a few things that we hope to see in the upcoming budget announcement. First, we would like to see the government increase their expenditures & deficit in order to invest more heavily into long-term growth initiatives. The Singapore government has run a large surplus for a long time, and it could definitely afford some deficit for the foreseeable future. This could come in form of continued investment into its infrastructure, as well as various tax reduction initiatives for corporates. It may be wise for them to even consider a meaningful tax cut for the consumers, which could have a positive impact on consumption and therefore the economy, and represented not even 1% of total expenditure for the government.

| S$ mn | FY2010 | FY2011 | FY2012 | FY2013 | FY2014 | FY2015 (Revised) | FY2016 (Budgeted) |

|---|---|---|---|---|---|---|---|

| Primary Surplus / (Deficit) | 722 | 4,514 | 6,811 | 5,292 | 4,190 | (4,246) | (4,986) |

| Basic Surplus / (Deficit) | (782) | 1,605 | 5,353 | 2,303 | 334 | (8,783) | (7,655) |

| Overall Budget Surplus / (Deficit) | 980 | 4,003 | 5,821 | 4,998 | 571 | (4,884) | 3,450 |

Secondly, we would like to see some increased investment in areas like education and technology. As you can see in our chart in the previous section, government’s development expenditure on education has declined from 22% of total spend in 2010 to 17% in 2016. At the same time, social & economic development expenditure on media, information and communication has fallen from 2.7% in 2010 to mere 1.6% in 2016. Education and technology are crucial in driving an economy’s long-term growth by upgrading the country’s talent level. Given the government’s recent interest in developing a booming hub for startups and technology companies, we are hopeful that the budget announcement may contain some increased investment in this area.

This article was first published at Valuepenguin.sg

Finance

CPF Special, MediSave, and Retirement accounts’ interest rate rises to 4.14% for Q4 2024

The Central Provident Fund (CPF) Board and Housing and Development Board (HDB) announced that the interest rate for CPF Special, MediSave, and Retirement accounts will increase to 4.14% in Q4 2024, up from 4.08%. The 4% floor rate will be extended for another year, providing members with stability amid a volatile interest environment, the announcement stated.

SINGAPORE: In a joint announcement on Friday (20 September), the Central Provident Fund (CPF) Board and the Housing and Development Board (HDB) revealed that the interest rate for CPF Special, MediSave, and Retirement accounts will rise to 4.14% for the fourth quarter of 2024, up from 4.08% in the previous quarter.

This increase, effective from October to December, comes as the pegged rate exceeds the established floor rate of 4%.

Finance

US taxation authority to pursue wealthy tax evaders with advanced AI tools

The Internal Revenue Service (IRS) of United States has announced a comprehensive initiative aimed at aggressively pursuing individuals and entities that owe substantial amounts in overdue taxes.

Under the initiative, 1,600 millionaires and 75 large business partnerships are the primary focus of the IRS’s intensified “compliance efforts.”

WASHINGTON, UNITED STATES: The Internal Revenue Service (IRS) announced last Friday (8 Sept), that it is embarking on an ambitious mission to aggressively target 1,600 millionaires and 75 large business partnerships that collectively owe hundreds of millions of dollars in overdue taxes.

IRS Commissioner Daniel Werfel revealed that with increased federal funding and the aid of cutting-edge artificial intelligence tools, the agency is poised to take robust action against affluent individuals who have been accused of evading their tax obligations.

During a call with reporters to provide a preview of the announcement, Commissioner Werfel expressed his frustration at the contrast between individuals who dutifully pay their taxes on time and those wealthy filers who, in his words, have “cut corners” when it comes to fulfilling their tax responsibilities.

“If you pay your taxes on time it should be particularly frustrating when you see that wealthy filers are not,” he said.

The IRS’s latest initiative targets 1,600 millionaires, each of whom owes a minimum of US$250,000 in back taxes, along with 75 large business partnerships boasting average assets of approximately US$10 billion.

These entities are now under the spotlight of the IRS’s renewed “compliance efforts.”

Werfel emphasised that a substantial hiring campaign and the implementation of artificial intelligence research tools, developed both by IRS personnel and contractors, will play pivotal roles in identifying and pursuing wealthy tax evaders.

This proactive approach by the IRS aims to highlight positive outcomes resulting from the increased funding it has received under President Joe Biden’s Democratic administration.

Notably, this move comes amid efforts by Republican members of Congress to reassess and potentially reduce the agency’s funding allocation.

IRS has introduced an extensive programme aimed at revitalisng fairness within the tax system

The IRS announced the groundbreaking move aimed at enhancing tax compliance and fairness, with a particular focus on high-income earners, partnerships, large corporations, and promoters who may be abusing the nation’s tax laws.

This initiative follows the allocation of funding under the Inflation Reduction Act (IRA) and a comprehensive review of enforcement strategies.

The new effort, which builds on the groundwork laid following last August’s IRA funding, will place increased attention on individuals with higher incomes and partnerships, both of which have experienced significant drops in audit rates over the past decade.

These changes will be facilitated through the implementation of advanced technology and Artificial Intelligence (AI) tools, empowering IRS compliance teams to more effectively detect tax evasion, identify emerging compliance challenges, and improve the selection of audit cases to prevent unnecessary “no-change” audits that burden taxpayers.

As part of the effort, the IRS will also ensure audit rates do not increase for those earning less than $400,000 a year.

Additionally, the agency will introduce new safeguards to protect those claiming the Earned Income Tax Credit (EITC).

The EITC is intended to assist workers with modest incomes, and despite recent years seeing high audit rates for EITC recipients, audit rates for individuals with higher incomes, partnerships, and those with complex tax situations have plummeted.

The IRS will also take measures to prevent unscrupulous tax preparers from exploiting individuals claiming these vital tax credits.

This move underscores the IRS’s commitment to fostering a fair and equitable tax system, ensuring that all taxpayers, regardless of income or complexity, are held to the same standards of compliance and accountability.

The initiative reflects a comprehensive approach to addressing disparities in tax enforcement and strengthening the integrity of the tax system for the benefit of all Americans.

“This new compliance push makes good on the promise of the Inflation Reduction Act to ensure the IRS holds our wealthiest filers accountable to pay the full amount of what they owe.

“The years of underfunding that predated the Inflation Reduction Act led to the lowest audit rate of wealthy filers in our history. I am committed to reversing this trend, making sure that new funding will mean more effective compliance efforts on the wealthy, while middle- and low-income filers will continue to see no change in historically low pre-IRA audit rates for years to come,”

“The nation relies on the IRS to collect funding for every critical government mission, from keeping our skies safe, our food safe and our homeland safe. It’s critical that the agency addresses fundamental gaps in tax compliance that have grown during the last decade,” Werfel said.

Major expansion in high-income/high wealth and partnership compliance work

Prioritisation of high-income cases: Under the High Wealth, High Balance Due Taxpayer Field Initiative, the IRS is intensifying efforts to address taxpayers with total positive income exceeding US$1 million and recognised tax debts of more than US$250,000.

Building on prior successes, which resulted in the collection of US$38 million from over 175 high-income earners, the IRS is allocating additional resources to focus on these high-end collection cases in Fiscal Year 2024.

The agency is proactively reaching out to approximately 1,600 taxpayers in this category who collectively owe substantial sums in taxes.

Expansion of pilot focused on largest partnerships leveraging Artificial Intelligence (AI): Recognising the complexity of tax issues in large partnerships, the IRS is expanding its Large Partnership Compliance (LPC) programme.

Leveraging cutting-edge Artificial Intelligence (AI) technology, the IRS is collaborating with experts in data science and tax enforcement to identify potential compliance risks in partnership tax, general income tax, accounting, and international tax.

By the end of the month, the IRS will initiate examinations of 75 of the largest partnerships in the United States, encompassing diverse industries such as hedge funds, real estate investment partnerships, publicly traded partnerships, large law firms, and more. These partnerships each possess assets exceeding US$10 billion on average.

Greater focus on partnership issues through compliance letters: The IRS has identified ongoing discrepancies in balance sheets within partnerships with assets exceeding US$10 million, indicating potential non-compliance.

Many taxpayers filing partnership returns are reporting discrepancies in the millions of dollars between year-end and year-beginning balances, often without attaching required explanations.

This effort aims to address balance sheet discrepancies swiftly, with an initial mailing of around 500 partnership notices set to begin in early October.

Depending on the response, the IRS will incorporate these cases into the audit process for further examination.

Priority areas for targeted compliance work in FY 2024

The IRS has launched numerous compliance efforts to address serious issues being seen. Some of these, like abusive micro-captive insurance arrangements and syndicated conservation easement abuses, have received extensive public attention. But much more work continues behind the scenes on other issues.

Among some of the additional priority areas the IRS will be focused on that will touch the wealthy evaders include:

Expanded work on digital assets: The IRS is continuing its expansion of efforts related to digital assets, encompassing initiatives such as the John Doe summons and the recent release of proposed broker reporting regulations.

The IRS’s Virtual Currency Compliance Campaign, which aims to ensure compliance with tax obligations related to digital currencies, will persist in the coming months.

An initial review has indicated a potential non-compliance rate of 75% among taxpayers identified through record production from digital currency exchanges.

The IRS anticipates the development of additional digital asset cases for further compliance efforts in early Fiscal Year 2024.

More scrutiny on FBAR violations: High-income taxpayers across various segments have been utilising foreign bank accounts to avoid disclosure and related tax obligations.

US individuals with a financial interest in foreign financial accounts exceeding US$10,000 at any point in the year are required to file a Report of Foreign Bank and Financial Accounts (FBAR).

The IRS’s analysis of multi-year filing patterns has revealed hundreds of potential FBAR non-filers with average account balances exceeding US$1.4 million. In response, the IRS plans to audit the most egregious potential non-filer FBAR cases in Fiscal Year 2024.

Labour brokers: The IRS has identified instances in which construction contractors are making payments to apparent subcontractors via Form 1099-MISC/1099-NEC, yet these subcontractors are, in fact, “shell” companies lacking a legitimate business relationship with the contractor.

Funds paid to these shell companies are routed through Money Service Businesses or accounts associated with the shell company before being returned to the original contractor. This scheme has been observed in states like Texas and Florida.

The IRS is expanding its attention in this area, conducting civil audits and launching criminal investigations to address non-compliance.

This effort is aimed at improving overall compliance, ensuring proper employment tax withholding for vulnerable workers, and creating a fairer playing field for contractors adhering to the rules.

Would DSP Jonathan Au Yong have filed a police report if he knew about Iswaran’s offences?

Al Jazeera documentary uncovers pro-Israel bias in western media coverage

SMRT cleans ‘spotty’ train flooring after Lim Tean’s public complaint

Four Bidadari flats sold for over S$1 Million after reaching MOP

Iswaran will not appeal 12-month jail sentence, accepts responsibility for his actions

Palestinian woman involved in disturbance at Wisma Transit Malaysia apologises

Macron calls for arms embargo on Israel, drawing sharp criticism from Netanyahu

Will Reddit post claiming 7 BTO failures be POFMAed?

Lim Chin Joo remembered for his contributions to Singapore’s anti-colonial movement

Lim Chin Joo, younger brother of Lim Chin Siong, passes away at age 87

TJC issued 3rd POFMA order under Minister K Shanmugam for alleged falsehoods

SDP: Chee Hong Tat, SMRT owe public full transparency, accountability for train system

-

Comments1 week ago

Comments1 week agoChristopher Tan criticizes mrt breakdown following decade-long renewal program

-

Comments7 days ago

Comments7 days agoNetizens question Ho Ching’s praise for Chee Hong Tat’s return from overseas trip for EWL disruption

-

Singapore1 week ago

Singapore1 week agoSMRT updates on restoration progress for East-West Line; Power rail completion expected today

-

Singapore2 weeks ago

Singapore2 weeks agoChee Hong Tat: SMRT to replace 30+ rail segments on damaged EWL track with no clear timeline for completion

-

Singapore1 week ago

Singapore1 week agoLee Hsien Yang pays S$619,335 to Ministers Shanmugam and Balakrishnan in defamation suit to protect family home

-

Singapore1 week ago

Singapore1 week agoTrain services between Jurong East and Buona Vista to remain disrupted until 1 Oct due to new cracks on East-West Line

-

Singapore2 weeks ago

Singapore2 weeks agoMajor breakdown on East-West Line: SMRT faces third service disruption in a month

-

Singapore2 weeks ago

Singapore2 weeks agoTransport Minister: Boon Lay-Queenstown train services may not resume tomorrow; SMRT leaders apologise