Foreign workers take four in five Singapore jobs in 2025 as internal indicators signal a turning cycle

Singapore added 55,500 jobs in 2025, but roughly four in every five went to non-resident workers. Beneath the headline, outward-facing sectors shifted into net contraction, PMET retrenchments exceeded pre-recessionary norms, and labour turnover hit historic lows. The data points to a labour market tight on paper but loosening beneath the surface.

- Roughly four in every five jobs added in 2025 went to non-resident workers, with foreign labour growth outpacing resident gains by nearly four to one.

- Outward-sector Employment Diffusion Index fell to 43.9 in 4Q 2025, shifting into net contraction territory even as headline employment grew.

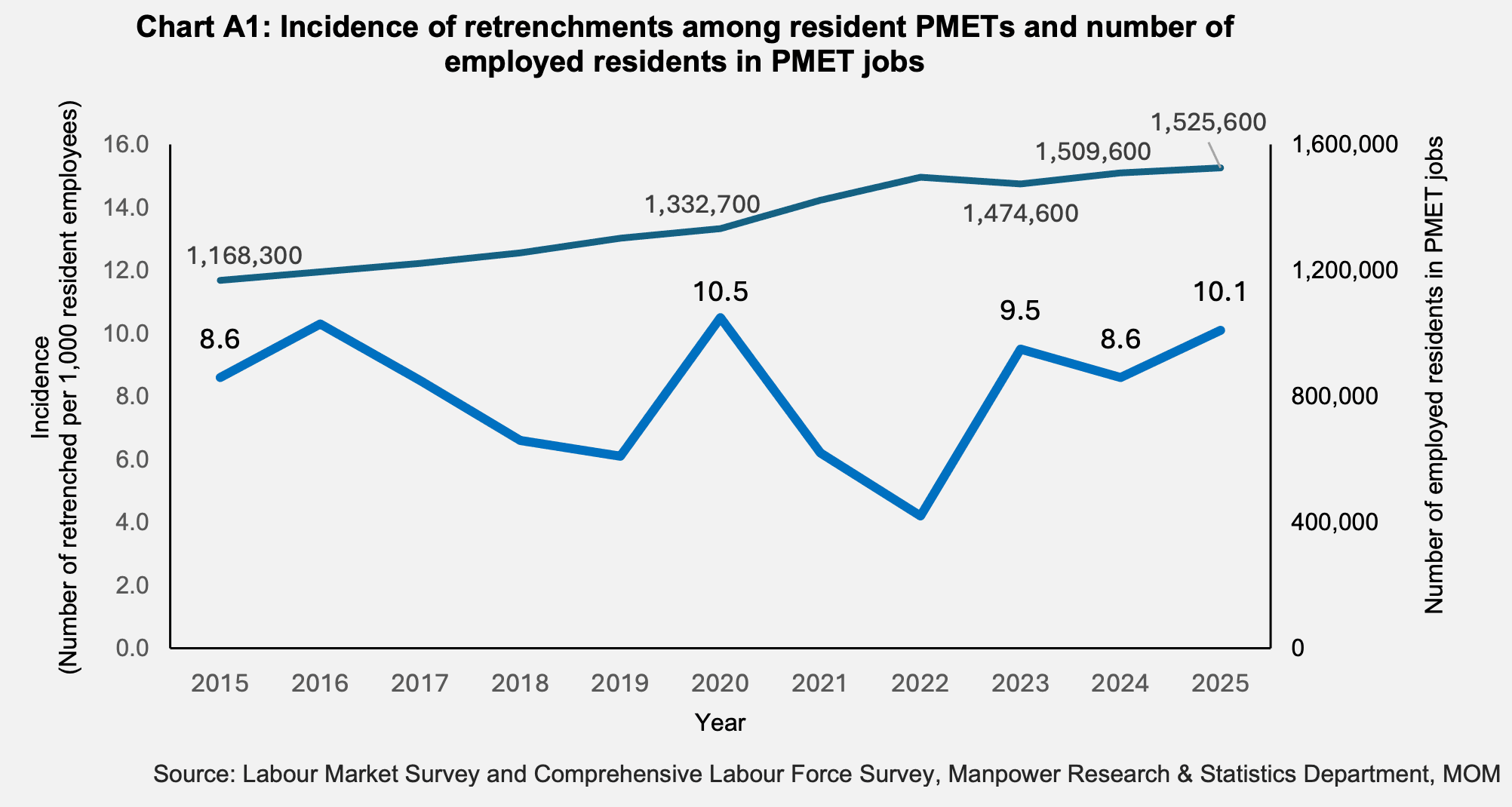

- PMET retrenchment incidence reached 10.1 per 1,000 resident employees in 2025, above the pre-recessionary norm, while Information and Communications employment declined outright.

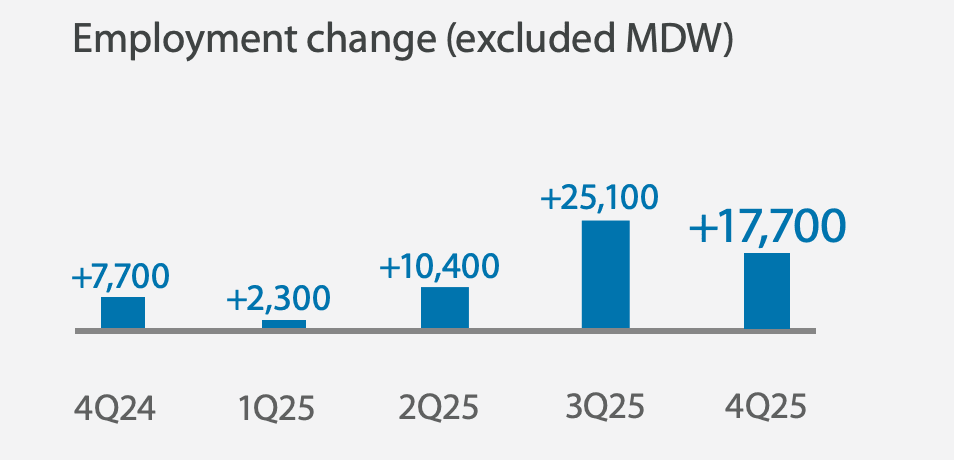

Singapore's labour market posted its 17th consecutive quarter of employment growth in the fourth quarter of 2025, with total employment expanding by 17,700 between October and December, according to the Ministry of Manpower (MOM)'s Labour Market Report Fourth Quarter 2025 released on 20 March 2026.

For the full year, 55,500 jobs were added — but roughly four in every five went to non-resident workers. Resident employment grew by 11,600 while non-resident employment grew by 43,900, a ratio of nearly four to one that the records but does not examine in depth.

The quarterly growth figure represents a sharp deceleration from the 25,100 recorded in 3Q 2025 — and that deceleration is not isolated. It coincides with a shift into net contraction among outward-facing sectors. Beneath the headline, professional workers faced retrenchment rates above pre-recessionary norms, part-time hours were quietly reduced, and labour turnover fell to historically low levels.

Taken together, these indicators point not to a labour market in decline, but to one that has likely moved past its peak rate of tightening.

Resident employment — covering Singapore citizens and Permanent Residents (PRs) — was concentrated in Financial Services and Health and Social Services, sectors requiring higher qualifications and longer training pathways. Non-resident growth was propelled almost entirely by Work Permit holders in Construction, where labour demand is physically intensive and project-driven.

These are not competing labour pools. Resident employment gains are concentrated in professional and healthcare roles requiring higher qualifications and longer training pathways. Non-resident gains are concentrated in construction and manufacturing, where labour demand is physically intensive, often project-driven, and structurally harder to fill from the resident workforce given Singapore's high resident labour force participation rate of 85.9% among those aged 25 to 64.

The ratio nonetheless raises longer-term questions. Non-resident employment grew at nearly four times the rate of resident employment. The report does not address the cumulative trajectory of this ratio across economic cycles, nor whether the structural dependence on non-resident labour in infrastructure-driven growth phases is being actively managed or simply reflected.

Breadth of employment growth is narrowing

Behind the headline employment figures, a key internal measure of labour market health deteriorated significantly in the fourth quarter.

The Employment Diffusion Index (EDI), which measures the share of industries recording net employment growth rather than contraction, fell from 58.9 in 3Q 2025 to 51.5 in 4Q 2025. An EDI reading above 50 means more sectors are expanding than contracting — but the margin has narrowed considerably.

More significantly, the EDI for outward-oriented sectors — which include Information and Communications, Manufacturing, Wholesale Trade, Transportation and Storage, Accommodation, Professional Services, and Financial and Insurance Services — fell from 56.1 in 3Q 2025 to 43.9 in 4Q 2025. A reading below 50 means more outward-facing sectors were contracting than expanding.

This is a material divergence. In previous quarters, employment growth was both strong and broad-based. In 4Q 2025, it remains strong but is no longer broad-based. Overall employment is still growing, but the engine of that growth is increasingly concentrated in domestic-oriented sectors, where the EDI held steady at 63.1 in both 3Q and 4Q 2025. Construction, driven by major infrastructure projects, and seasonal hiring in Administrative and Support Services and Retail Trade account for a significant share of 4Q employment growth.

Some of that seasonal growth is by definition temporary. The report notes that fourth-quarter gains in Administrative and Support Services and Retail Trade were driven by holiday and events hiring. A portion of the employment expansion recorded in December 2025 will not carry forward into the first quarter of 2026.

The narrowing breadth of growth, the net contraction reading in outward sectors, and the partial reliance on seasonal hires together suggest that the headline employment figure is a less reliable indicator of underlying labour market strength than it has been in previous quarters.

Unemployment stable, with early signs of pressure among younger residents and degree holders

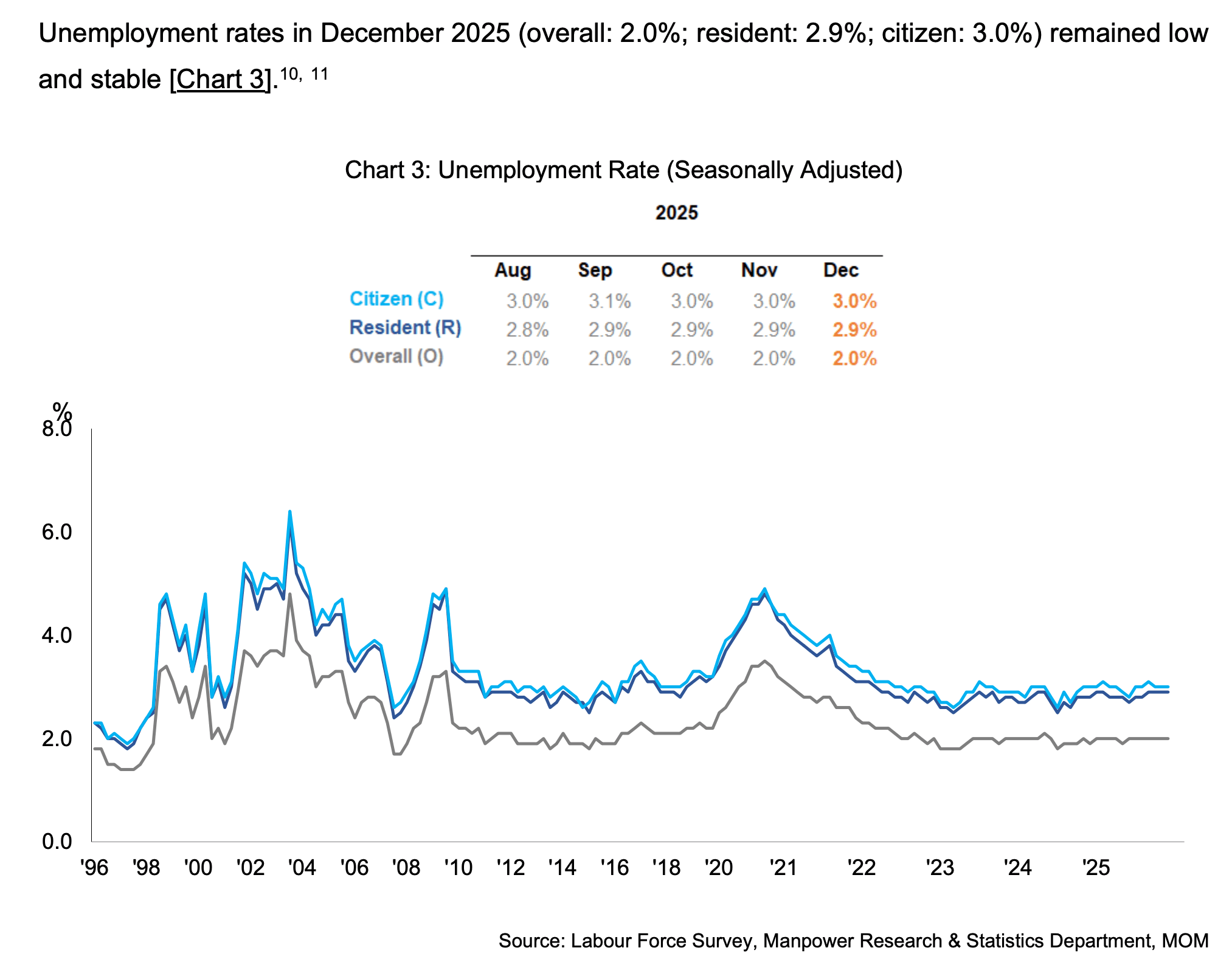

Unemployment rates in December 2025 held steady at 2.0% overall, 2.9% for residents and 3.0% for citizens — consistent with September 2025 figures and within long-established low ranges.

The resident long-term unemployment rate, which captures those out of work for 25 weeks or more, remained stable at 0.9% in December 2025.

Within these aggregates, however, early signs of pressure are emerging by age and education. Unemployment among residents aged below 30 edged up from 5.6% in September 2025 to 5.8% in December 2025, a level last seen in March 2024. The report notes this rise is more contained than comparable increases in advanced economies such as the United States, France and Germany, and these figures remain within recent cyclical ranges rather than representing a structural break.

Long-term unemployment among residents below 30 also rose, from 1.3% in September 2025 to 1.5% in December 2025. Among degree holders, long-term unemployment increased from 1.0% to 1.1% over the same period. The report suggests these jobseekers are taking longer to find roles that match their skills and salary expectations, which may also reflect a structural mismatch in graduate-level hiring that the available data does not yet fully resolve.

Separately, the unemployment rate for residents aged 60 and above declined for the third consecutive quarter, from 2.1% to 1.7% in December 2025, signalling improving employment prospects for older workers.

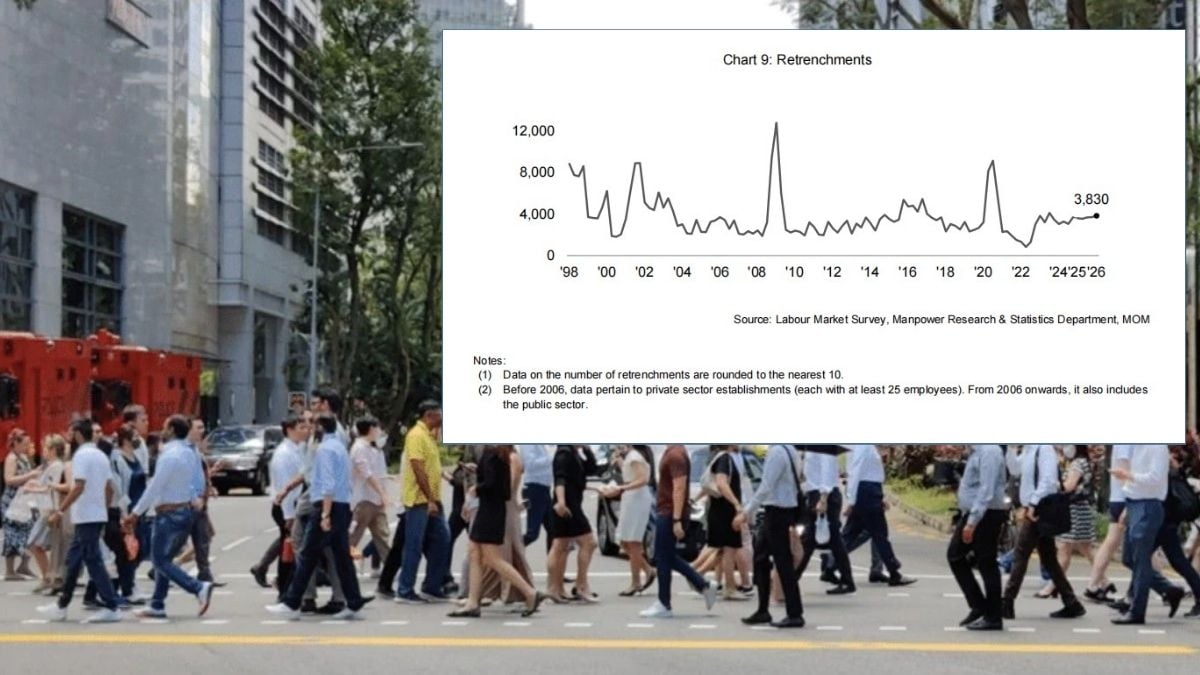

Retrenchments low in aggregate, but PMET incidence crosses pre-recessionary threshold — and I&C employment is shrinking

Retrenchments in 4Q 2025 totalled 3,690, equivalent to 1.5 retrenched per 1,000 employees — within the non-recessionary ten-year quarterly average and below the 1.7 per 1,000 recorded as the pre-COVID norm between 2014 and 2019. For the full year 2025, 14,490 workers were retrenched, up from 13,020 in 2024. Business reorganisation and restructuring accounted for 75.2% of all retrenchment reasons in 4Q 2025.

The system-wide retrenchment picture therefore remains contained. The distribution of retrenchment by occupational group, however, tells a different story.

For the full year 2025, the incidence of retrenchment among resident PMETs reached 10.1 per 1,000 resident employees — above the pre-recessionary benchmark of 8.0 established between 2015 and 2019. Financial Services, Information and Communications and Professional Services recorded the highest PMET retrenchment numbers.

PMET employment continues to rise in aggregate, but within that aggregate, high-skill sectors such as Information and Communications are already contracting. I&C employment recorded a marked decline in 2025 after growing in 2024 — a contraction in a sector that is simultaneously the most PMET-intensive and most exposed to AI-driven restructuring. That the sector recording this decline is also the one where PMET displacement anxiety is highest is a conjunction the report does not explicitly address.

The report characterises the overlap between high retrenchments and high PMET vacancies in the same sectors as evidence of restructuring rather than demand contraction. The overall PMET job vacancy to unemployed ratio remained above one at 1.11. Whether retrenchment and re-hiring in the same sectors reflects genuine workforce renewal or a systematic downshift in the seniority and compensation of roles being filled is not examined.

Residents formed 77.7% of all retrenched employees in 4Q 2025. Approximately nine in ten received retrenchment benefits, with close to eight in ten receiving the recommended minimum of two weeks of salary per year of service.

Hidden slack: part-time hours cut, short work-weeks rising

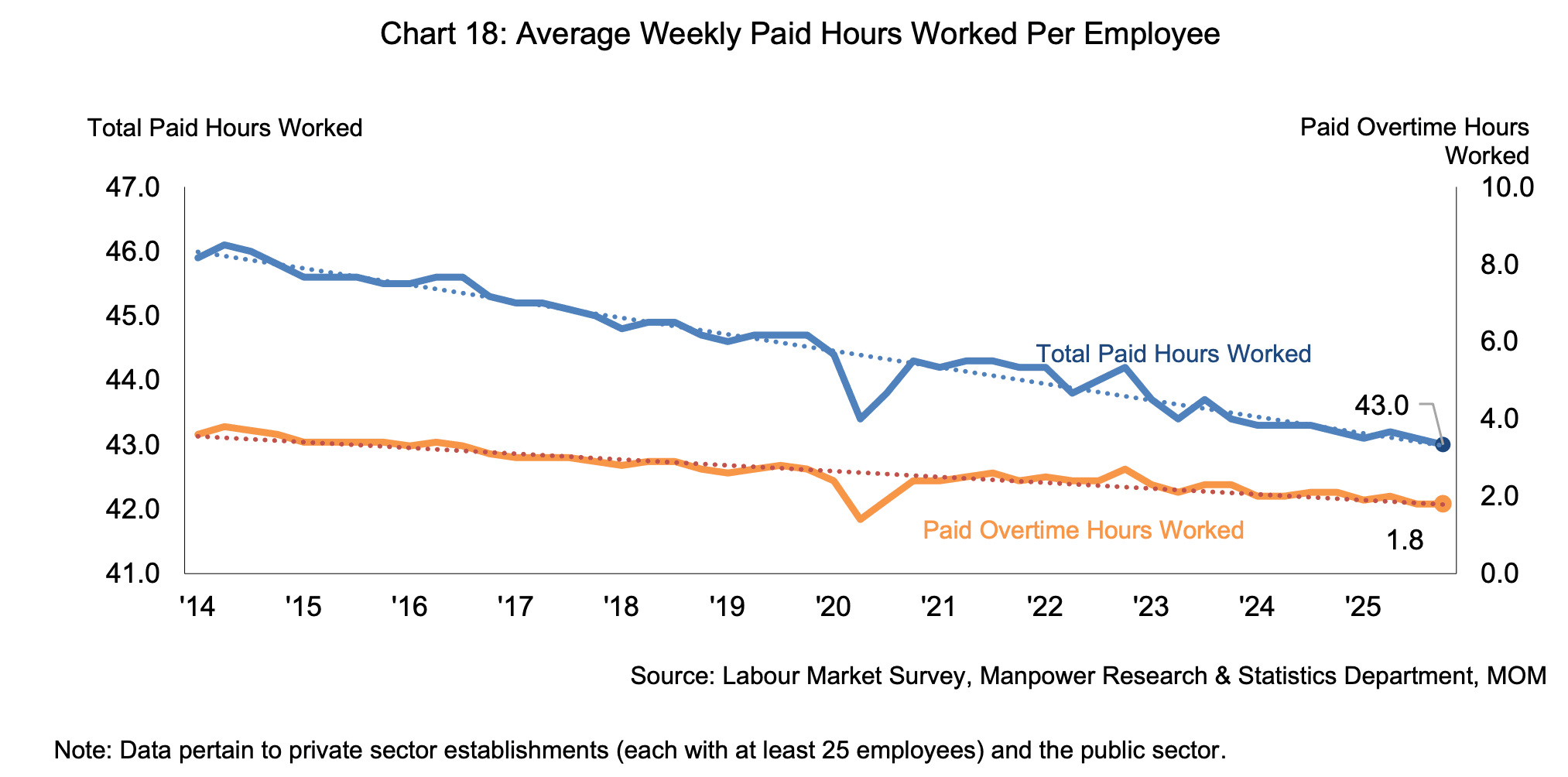

A more precise indicator of how firms are managing labour costs quietly emerged from the hours-worked data. In December 2025, average weekly paid hours among part-time employees fell from 26.4 hours to 25.2 hours over the quarter, while full-time hours held flat at 44.2 hours. Paid overtime hours for part-timers remained negligible.

The pattern indicates that firms are reducing hours at the intensive margin rather than the extensive margin — adjusting the hours of existing flexible and part-time workers rather than cutting permanent headcount. This is a classic early-stage adjustment that does not register in headline employment or retrenchment figures.

This reading is reinforced by the parallel trend in short work-week placements, which rose for the third consecutive quarter: 620 in 2Q 2025, 800 in 3Q 2025, and 960 in 4Q 2025. Most of those affected in 4Q 2025 were on reduced-hours arrangements (680) rather than temporary layoffs (280). Non-PMETs accounted for approximately 68.5% of those on short work-week arrangements.

Taken together — falling part-time hours, rising short work-weeks, and a third consecutive quarterly increase in the latter — the picture is one of firms applying gradual, quiet pressure on flexible labour rather than committing to outright retrenchment. The report contextualises the short work-week figures against the pandemic peak of 72,690 in 2020, a comparison that may understate the significance of the recent upward trend. The relevant comparison is the directional trend, which is uniformly upward.

Job vacancies exceed unemployed persons; construction drives December surge

Job vacancies rose from 69,600 in September 2025 to 77,700 in December 2025, reversing a dip from the June 2025 figure of 76,200. The job vacancy to unemployed persons ratio increased from 1.50 to 1.58 over the same period.

The December increase was driven primarily by Construction, reflecting manpower demand tied to major infrastructure projects including Terminal 5 and the Marina Bay Sands expansion. Vacancies also rose in I&C, Professional Services and Health and Social Services, but moderated in Food and Beverage Services and Transportation and Storage.

For the full year 2025, the annual average of job vacancies stood at 75,900, slightly above the 2024 average of 75,400.

The coexistence of a rising vacancy ratio with low hiring intent and falling resignation rates raises a deeper question. Measured labour demand — as captured by vacancy numbers — is not translating into actual labour market dynamism. Firms are posting vacancies but not hiring aggressively. Workers are not resigning to take them. The vacancy ratio, read in isolation, suggests a tight market. Read alongside turnover and hiring intent data, it suggests a market in which demand and supply are both present but neither side is moving with conviction.

A growing structural concern embedded in the data is the share of PMET vacancies remaining unfilled for six months or more, which rose from 14.4% in 2024 to 16.0% in 2025. Employers cited difficulty sourcing candidates with specialised technical skills, including data scientists, teaching professionals and civil engineers.

Low labour turnover contradicts tight market framing

The Ministry of Manpower's characterisation of Singapore's labour market as one where demand "remains firm" is complicated by the labour turnover data, which tells a quieter story.

In 4Q 2025, the average monthly recruitment rate rose modestly to 2.0% and the resignation rate to 1.3% — slight increases from the previous quarter but both below historical averages, continuing a general downtrend over the decade.

Low resignation rates are not a sign of contentment in isolation. They typically indicate that workers do not feel confident enough to leave for better opportunities. In a genuinely tight labour market, resignation rates tend to rise as employees exercise leverage. The fact that resignations remain historically subdued — even as GDP grew 5.0% in 2025 and job vacancies outnumbered job seekers — suggests workers are not translating headline conditions into bargaining power.

Low recruitment rates, meanwhile, indicate that firms are not aggressively expanding headcount despite positive sentiment surveys. The proportion of firms planning to hire in the next three months stood at 43.3% in December 2025, below levels seen in the preceding two years.

The combination of low resignations and subdued recruitment points to a labour market in which both sides — workers and employers — are exercising caution simultaneously. That dynamic is inconsistent with a tight market in the conventional sense, and more consistent with a period of watchful stasis: employment is stable, but momentum is not building.

Higher turnover was concentrated in lower-skilled segments of Administrative and Support Services, particularly Security and Investigation and Cleaning and Landscaping, where barriers to entry are low and workers move more readily between employers.

Re-entry into employment improves, with most workers recovering wages

The resident rate of re-entry into employment six months after retrenchment rose from 55.4% in 3Q 2025 to 57.4% in 4Q 2025. Among those retrenched 12 months earlier, 68.9% had secured new employment by 4Q 2025.

Improvements were recorded across most occupational and educational groups. Among PMETs, the six-month re-entry rate rose from 54.3% to 56.4%. Degree holders recorded an increase from 51.3% to 53.9%, ending three consecutive quarters of decline — though their re-entry rate remains the lowest among all educational groups.

The mean time to re-employment within six months was 2.6 months in 2025, up marginally from 2.5 months in 2024. Approximately six in ten retrenched workers who re-entered employment received similar or higher wages than in their previous roles. Workers leaving Financial Services, I&C and Professional Services were most likely to achieve full wage recovery.

One figure the report does not contextualise: a 57.4% six-month re-entry rate also means that roughly four in ten retrenched residents had not secured new employment within six months of losing their jobs.

Outlook cautious, business hiring expectations subdued

The Ministry of Trade and Industry (MTI) upgraded Singapore's gross domestic product (GDP) growth forecast for 2026 from a range of 1.0% to 3.0% to a revised range of 2.0% to 4.0% in February 2026, following stronger-than-expected global growth in 4Q 2025. The Singapore economy grew 6.9% year-on-year in 4Q 2025 and 5.0% for the full year 2025.

Despite the revised forecast, business sentiment on hiring remains cautious. Wage expectations were similarly subdued, with only 26.4% of firms indicating intentions to raise wages — below levels seen in the preceding two years. The proportion of firms intending to raise wages stood at 26.4%, also below recent historical norms.

The report projects that retrenchments may edge upward in outward-oriented sectors in early 2026 but expects them to remain within non-recessionary levels. Unemployment rates are expected to remain low and stable throughout the year.

Resident employment is projected to grow at a similar or slightly slower pace than 2025, given Singapore's already high resident labour force participation rate. Non-resident employment growth is expected to continue outpacing resident gains.

The labour market is not weakening in headline terms. But its internal indicators — breadth of growth, hours worked, turnover, and sectoral composition — suggest a cycle that is no longer tightening, but quietly turning at the margin.