MAS keeps S$NEER policy unchanged, raises 2026 inflation outlook

MAS left monetary policy unchanged on 29 January 2026, citing resilient growth and inflation pressures returning closer to trend, while raising its 2026 inflation forecasts to 1–2 per cent.

- MAS will maintain the current rate of appreciation, width, and centre of the S$NEER policy band.

- Inflation forecasts for 2026 were raised, with both core and headline inflation expected at 1–2 per cent.

- Growth is expected to remain resilient in 2026, supported by AI-related investment and firm domestic sectors.

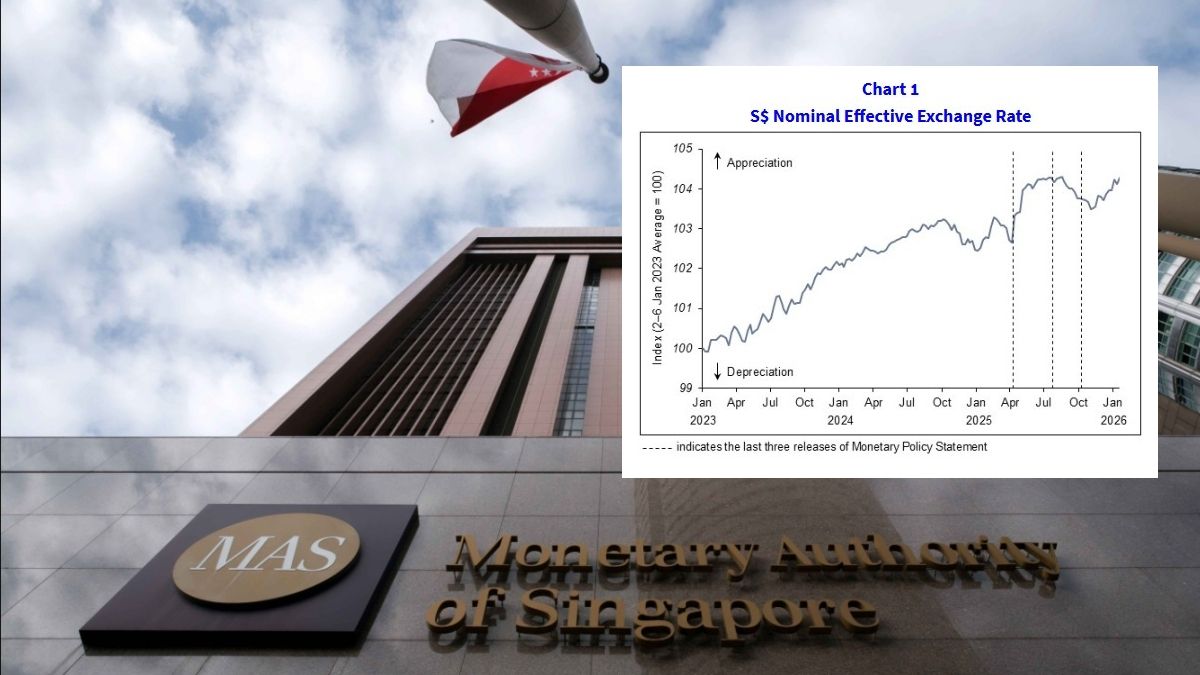

SINGAPORE: The Monetary Authority of Singapore (MAS) will maintain the prevailing rate of appreciation of the Singapore dollar nominal effective exchange rate (S$NEER) policy band.

In its monetary policy statement dated 29 January 2026, the central bank said it would also keep the band’s width and the level at which it is centred unchanged.

MAS said the current policy stance leaves it “in an appropriate position to respond effectively to any risk to medium-term price stability”.

The central bank added that it would continue to closely monitor economic developments amid uncertainties in the external environment.

Alongside the unchanged policy decision, MAS raised its inflation forecasts for 2026.

It now expects both core inflation and headline CPI-All Items inflation to come in between 1 per cent and 2 per cent.

This represents an upward revision from the previous forecast range of 0.5 per cent to 1.5 per cent announced in October 2025.

MAS Core Inflation excludes accommodation and private road transport.

Drivers of core inflation: wages and productivity

The central bank said core inflation is expected to increase modestly in the near term.

This would reflect a pick-up in services unit labour costs after a subdued pace earlier in 2025.

However, MAS noted that recent improvements in services productivity could be sustained, helping to dampen the extent of cost increases.

Imported inflation is expected to remain contained.

MAS said global oil and food commodity prices are projected to decline in 2026, although at a progressively slower pace over the quarters.

Regional consumer price inflation is also forecast to edge up only slightly, with subdued producer prices in Asia continuing to limit cost pressures.

On balance, MAS said risks to the growth and inflation outlook are “tilted to the upside at this point”.

Persistently stronger-than-expected economic growth could lead to higher wage growth and boost consumer sentiment.

This, in turn, could exacerbate demand-driven inflationary pressures.

Supply-side risks are also present.

MAS said geopolitical developments could trigger supply shocks, raising imported costs and adding to inflation pressures.

At the same time, the central bank highlighted downside risks to the outlook.

A sharp correction in global financial markets or an abrupt pullback in artificial intelligence-related investment could cause growth to ease more quickly.

Such a scenario would likely result in lower inflation.

Resilient growth underpins policy decision

MAS said Singapore’s economic growth is expected to remain resilient in 2026.

It added that underlying price pressures are returning closer to historical trends.

These conditions supported its decision to maintain the existing S$NEER policy settings.

External environment: AI investment and global trade

The central bank noted that economic activity in Singapore’s major trading partners remained resilient in the final quarter of 2025.

This was supported by the global AI-related investment boom and a reduction in trade policy uncertainty.

Looking ahead, MAS expects global growth to ease modestly.

The central bank said the lagged effects of higher tariffs are likely to weigh on final demand and trade.

However, the extent of the moderation could be mitigated by supportive fiscal and monetary policies in major economies.

MAS also expects the global AI capital expenditure upcycle to continue.

Domestic growth momentum stronger than expected

Domestically, advance estimates from the Ministry of Trade and Industry show that Singapore’s economy grew by 1.9 per cent on a quarter-on-quarter, seasonally adjusted basis in the fourth quarter of 2025.

This followed a 2.4 per cent expansion in the preceding quarter.

MAS said the outcome was stronger than expected.

Growth was driven by robust performance in manufacturing and services segments closely tied to the global technology cycle.

In the near term, MAS expects Singapore’s GDP growth to remain resilient, although uncertainties persist.

Trade-related sectors are likely to be supported by continued near-term strength in the global AI-driven capital expenditure cycle.

Non-technology-related segments are also forecast to perform steadily.

MAS said financial services should benefit from stable lending activity and capital market flows.

The construction sector is expected to be supported by an ongoing pipeline of public and private sector projects.

For the full year, however, MAS expects GDP growth to ease compared with the stronger outturn in 2025.

The positive output gap is projected to narrow gradually over the course of 2026.

Recent inflation trends and policy background

On inflation trends, MAS said core inflation rose to 1.2 per cent year on year in the fourth quarter of 2025.

This was up from 0.4 per cent in the preceding quarter.

The increase partly reflected higher private health insurance premiums and holiday-related expenses.

The dissipation of base effects from enhanced subsidies also contributed to the rise.

Beyond these temporary factors, MAS said inflation momentum picked up across most core goods and services.

This was in line with rising regional prices and domestic wage growth.

For 2025 as a whole, MAS Core Inflation averaged 0.7 per cent.

This was significantly lower than the 2.8 per cent recorded in 2024.

MAS manages monetary policy through the exchange rate rather than interest rates.

The Singapore dollar is allowed to move within an undisclosed policy band against the currencies of major trading partners.

Policy adjustments can be made by changing the slope, width, or mid-point of the band.

Last year, MAS eased monetary policy in January and April 2025.

It subsequently kept policy unchanged in July and October.