MAS warns hiring may slow and wage growth ease amid Middle East conflict uncertainty

Singapore’s central bank warns firms may slow hiring and trim wage increases in 2026 as Middle East conflict risks weigh on growth and inflation outlook.

- Hiring and wage growth in 2026 are expected to moderate amid economic uncertainty.

- Energy shocks and inflation risks could weigh on growth and labour market conditions.

- Domestic and modern services sectors continue to support resident employment demand.

Singapore’s labour market is expected to soften in 2026 as geopolitical tensions weigh on economic prospects, with companies likely to adopt a more cautious approach to hiring and salary increases, according to the Monetary Authority of Singapore (MAS).

In its latest quarterly macroeconomic review released on 14 April 2026, MAS said growing uncertainties stemming from the Middle East conflict are already affecting business sentiment and could dampen employment momentum.

Business outlook weakens

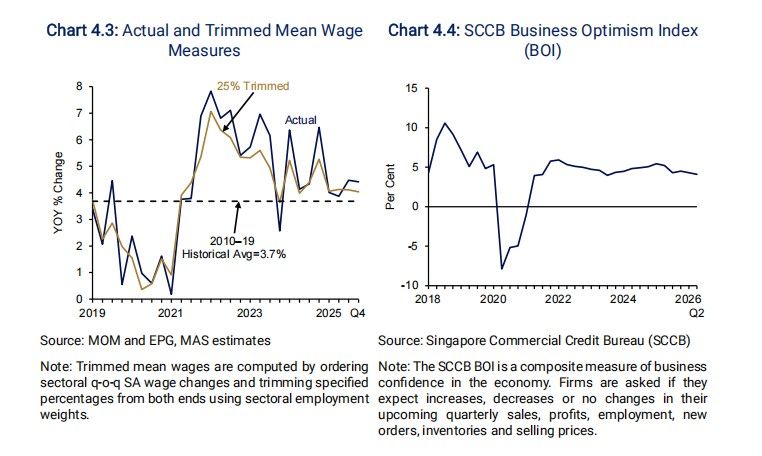

MAS cited a business optimism index by the Singapore Commercial Credit Bureau, noting that overall sentiment has “softened slightly” during the conflict.

“With the anticipated slowing of the economy, employment growth is expected to ease from the gains in 2025, with non-resident employment growth adjusting in tandem,” the central bank said.

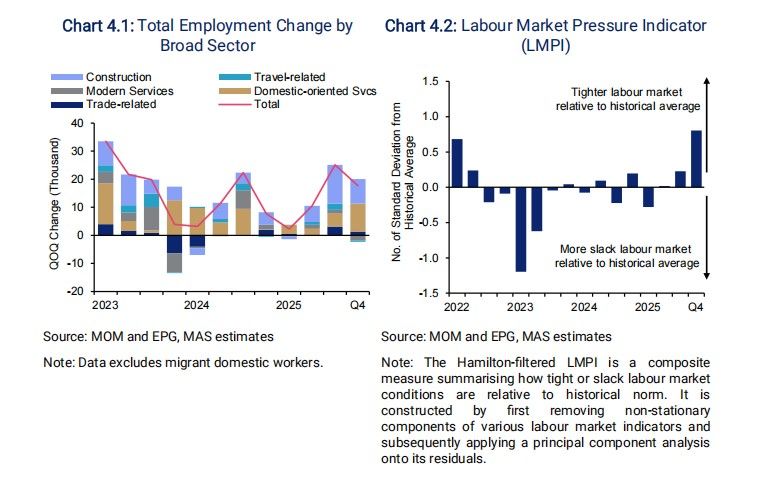

Despite the moderation, resident employment is expected to remain supported by hiring in domestic-oriented and modern services sectors.

Sectors such as health and social services, public administration and education continue to show “structurally sound” labour demand, the report noted.

At the same time, vacancies persist for skilled workers in technology and engineering roles, reflecting ongoing structural demand driven by rapid technological development.

Uneven impact across industries

MAS said sectors more exposed to energy shocks may pull back on hiring, although overall labour market conditions are expected to remain broadly balanced.

Nominal wage growth for residents is projected to moderate compared with 2025, reflecting softer labour market conditions.

However, pre-announced salary adjustments and policy-driven increases, including those under the Progressive Wage Model, are expected to provide some support.

The central bank warned that a deeper or more prolonged slowdown could worsen labour market outcomes.

“Hiring plans could be scaled back more substantially and retrenchments could rise, along with a more pronounced moderation in wage growth,” MAS said.

Recent labour market trends

The latest projections follow a relatively strong performance in the second half of 2025.

Total employment rose by 17,700 in the fourth quarter, with nearly half of the annual increase driven by non-resident construction workers.

Excluding construction, employment growth remained stable, while resident employment expanded at a firmer pace compared with 2024, according to the data provided by MAS.

Growth among residents was concentrated in domestic-oriented services and modern services sectors, including retail, food and beverage, and administrative support services.

The report comes shortly after ministerial statements in parliament addressing Singapore’s response to the Middle East conflict.

Manpower Minister Dr Tan See Leng previously said supporting fresh graduates remains a priority, particularly as artificial intelligence disruptions reshape the labour market.

He indicated that removing foreign worker levies could be counterproductive, even as energy costs rise.

Inflation and growth risks

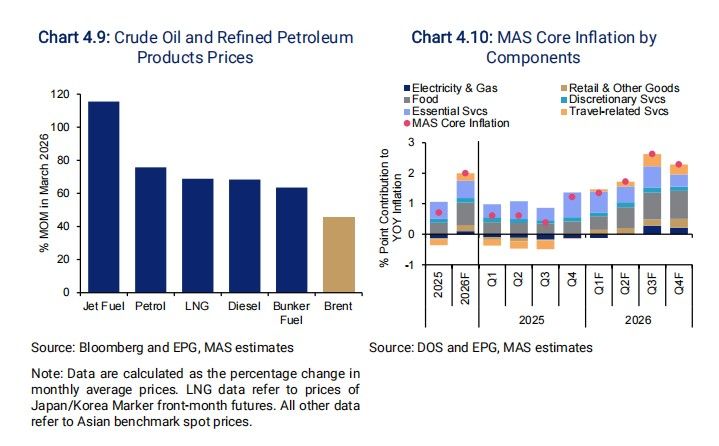

MAS said inflation is expected to “ease progressively” into 2027, in line with global energy price trends.

However, risks remain tilted to the upside due to potential disruptions in energy supply.

“A prolonged disruption to global energy supplies or the unexpected implementation of export controls would lead to even higher import costs for Singapore,” the central bank said.

Rising import prices could erode household real incomes and dampen overall demand.

Economic growth is also expected to slow in 2026, stepping down from the 5 per cent recorded in 2025.

The slowdown is projected to be broad-based, with the output gap averaging around zero per cent.

Sectoral pressures from energy shocks

Energy-dependent industries are expected to face the greatest strain.

These include petroleum, gas, electricity, petrochemicals, transportation, and water services, each with energy inputs exceeding 10 per cent of total requirements.

The chemicals sector has already been affected by disruptions to critical inputs, with potential spillover effects to other industries.

Wholesale trade, which accounts for 19 per cent of GDP, is particularly exposed due to its reliance on energy-intensive transport and storage services.

Domestic sectors are also facing rising costs.

Land transport operators are directly affected, while construction firms report higher petroleum-based material costs.

Food and beverage businesses may encounter increased expenses for utilities, packaging, and raw materials.

Technology and AI vulnerabilities

While artificial intelligence demand remains robust, MAS warned that supply chain disruptions could pose risks.

The Middle East plays a key role in producing helium, a critical input for semiconductor manufacturing.

Supply shortages could drive up prices for servers and networking equipment, increasing costs for data centres.

“Continued uncertainty and a higher inflationary environment could also affect investment sentiment in the AI ecosystem,” MAS said.

Global economic implications

MAS described the current energy shock as potentially more systemic and prolonged than previous crises.

A sustained disruption could trigger “disorderly corrections” in asset prices and lead to sharper declines in global growth.

In such a scenario, inflation could remain elevated in 2026 even as economic activity weakens.

Countries with limited fiscal and energy buffers would be most vulnerable, while financial market contagion could amplify risks.

“All in, the impact from the Middle East conflict will weigh on Singapore’s economic activity in the coming quarters, although the extent remains uncertain given the evolving developments,” MAS said.