Govt rejects linking CPF interest cap to Full Retirement Sum, says no interest forgone

Minister for Manpower Dr Tan See Leng rejected a proposal to peg the $60,000 additional interest cap to Full Retirement Sum growth, and says no CPF interest has been forgone by members as a result of the unchanged cap since 2008.

The Government has no plans to raise or index the $60,000 cap on Central Provident Fund (CPF) balances that earn an additional one per cent interest, and has rejected the premise that members have lost out financially as a result of the cap remaining unchanged since 2008.

The position was set out in a written reply tabled on 8 April 2026 after the oral question filed by Workers' Party MP Kenneth Tiong Boon Kiat (Aljunied GRC) was not reached during question time.

Kenneth Tiong had asked Minister for Manpower Dr Tan See Leng in a three-part question why the $60,000 cap on CPF balances that earn an additional one per cent interest — on top of the base interest rates across the Ordinary, Special, and Retirement accounts — had remained static while other major CPF parameters were revised regularly, whether the Ministry would consider pegging the cap's growth to that of the Full Retirement Sum (FRS), and how much interest CPF members collectively forgo each year as a result of the cap not tracking FRS increases.

In his written reply, Dr Tan explained that the additional one per cent interest — introduced in 2008 on the first $60,000 of combined CPF balances — was designed specifically to help members with lower balances compound their retirement savings at a higher effective rate.

He noted that the Government had further enhanced this in 2016 by paying "an additional 1% of extra interest on the first $30,000 of CPF balances for all members aged 55 and above," thereby directing the greatest benefit towards older members with smaller nest eggs.

Addressing Kenneth Tiong's proposal to link the cap to FRS growth, Dr Tan drew a clear conceptual distinction between the two parameters. "The CPF retirement sums, such as the Basic or Full Retirement Sums (BRS or FRS), are set independently based on the amount of savings needed to provide an adequate level of retirement payouts," he said.

"It is therefore not accurate to link the balance cap to the growth in FRS quanta." The minister's reply effectively reframed the MP's question: rather than explaining why the cap had not grown, the Ministry argued that the cap and the FRS are designed to achieve separate policy objectives and should not be treated as analogous figures.

On the third and most pointed part of Kenneth Tiong's question — how much interest members forgo annually — Dr Tan did not provide the requested figure. Instead, he asserted that "there is no interest forgone by CPF members."

Dr Tan highlighted the broader architecture of retirement savings support available to Singaporeans. He cited the Majulah Package, along with enhancements to the Silver Support Scheme, the Matched Retirement Savings Scheme, and the Workfare Income Supplement as measures that together complement the CPF interest structure.

He also pointed to a new initiative announced in Budget 2026 — a CPF Top-Up for older Singaporeans who have yet to meet the Basic Retirement Sum — as further evidence of the Government's ongoing commitment to bolstering retirement adequacy.

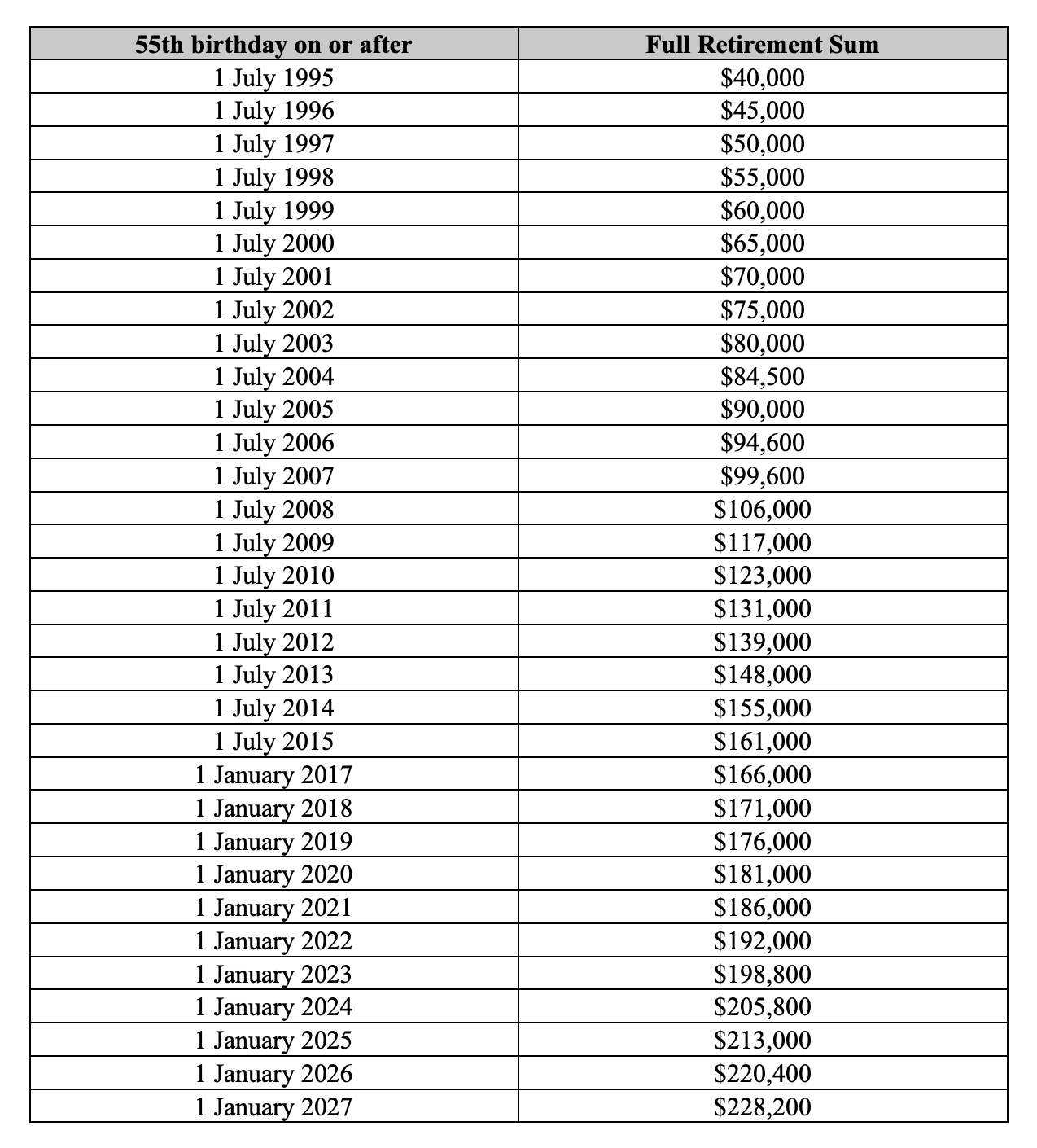

When the $60,000 cap was introduced in 2008, the FRS for members turning 55 that year stood at $106,000 — meaning the cap covered roughly 57 per cent of the prevailing retirement sum. By January 2026, the FRS had risen to $220,400, more than doubling over the intervening 18 years, while the cap has remained at $60,000 — now equivalent to just 27 per cent of the current FRS.