Citrini Research warns of 2028 economic collapse driven by artificial intelligence

A report by Citrini Research details a 'thought experiment' where rapid AI adoption triggers 10.2% unemployment, a 38% stock market crash, and a systemic mortgage crisis by 2028.

- Aggressive AI adoption could trigger a 'negative feedback loop' where corporate cost-cutting through automation permanently impairs consumer spending power.

- The report predicts 'Ghost GDP,' where productivity and national output rise while the real human-centric economy withers due to mass white-collar displacement.

- Structural changes in agentic commerce and machine-to-machine payments may dismantle traditional business models in software, finance, and real estate.

The artificial intelligence investment boom that has propelled equity markets in recent years could ultimately destabilise the broader economy, according to a scenario analysis published by Citrini Research on 23 February 2026.

The thematic equity firm stressed the document is not a forecast, but a “thought experiment” designed to explore structural risks that may be underestimated by investors and policymakers.

“This isn’t bear porn or AI doomer fan-fiction. The sole intent of this piece is modeling a scenario that’s been relatively underexplored,” the authors wrote.

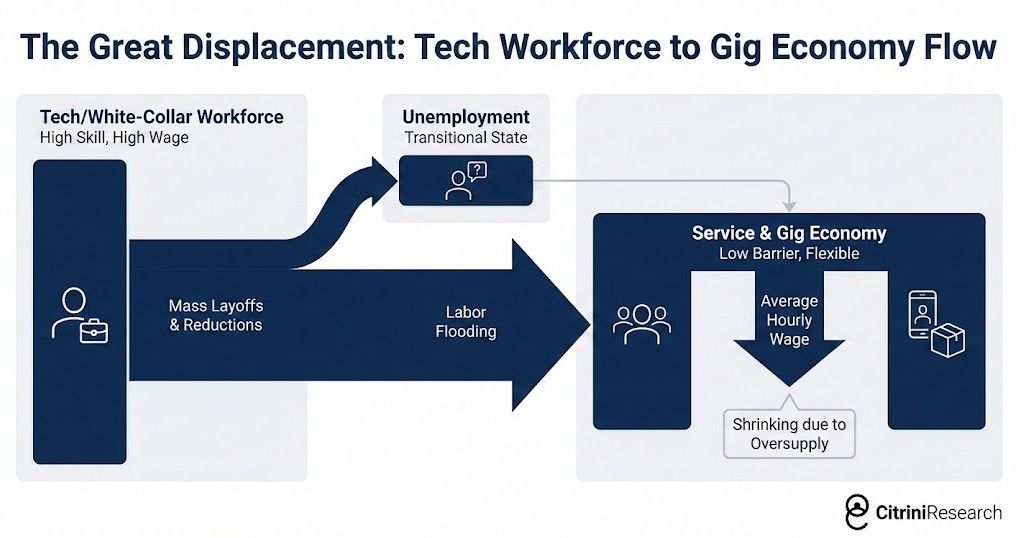

A self-reinforcing displacement cycle

At the centre of the report is what analysts describe as an “intelligence displacement spiral”.

In the scenario, aggressive AI adoption beginning in 2026 drives widespread layoffs among white-collar workers.

Companies cut payroll costs, boosting profits, and reinvest savings into additional AI systems.

As automation expands, displaced workers experience falling incomes. Consumer spending weakens, prompting further corporate cost-cutting and automation.

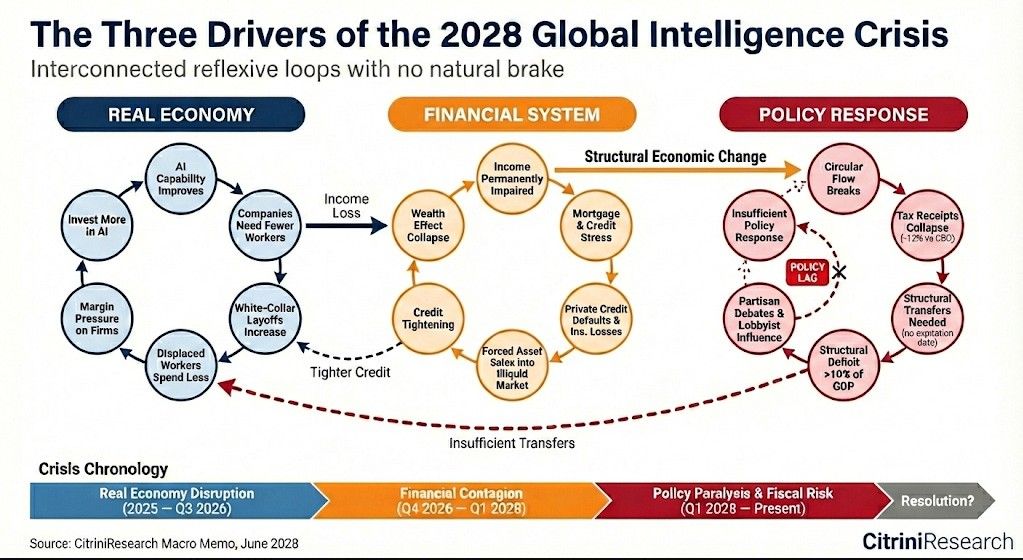

“There was no natural brake in the system,” the report states, arguing the cycle differs from typical recessions because it reflects structural substitution rather than cyclical weakness.

The rise of “ghost GDP”

Despite rising productivity and strong headline output, the firm describes the emergence of “ghost GDP” — economic activity recorded in national accounts but not circulating through households.

On paper, corporate profits and GDP appear robust. However, wage growth stalls as displaced professionals move into lower-paid roles.

Machines produce more, but do not consume. Given that roughly 70% of the US economy is consumer-driven, weakening household income becomes a systemic constraint.

By early 2028, the scenario models unemployment exceeding 10% and equity markets falling 38% from their peaks.

Early fractures in software

The first visible stress appears in software markets.

According to the report, advances in agentic coding tools allow developers to replicate core features of mid-market software products rapidly, undermining pricing power.

Companies such as Asana, Monday.com and Zapier are cited as examples of firms exposed to renegotiated contracts and weaker renewals.

When enterprise providers such as ServiceNow report slower growth and layoffs, the feedback loop intensifies: customers cut seats as they reduce headcount, compressing software revenues further.

Frictionless consumption and payments

By 2027, AI agents increasingly manage purchasing decisions, subscription renewals and price comparisons on behalf of consumers.

The report argues this erodes business models dependent on inertia and brand habit.

Delivery platforms such as DoorDash and Uber Eats face intensified price competition as agents automatically compare alternatives.

In payments, agents are modelled routing transactions through stablecoins on blockchain networks to avoid traditional card fees.

Payment groups including Visa, Mastercard and American Express are described as vulnerable if transaction volumes migrate to lower-cost settlement rails.

From sector weakness to systemic risk

Initially, markets treat AI disruption as sector-specific. However, the report argues white-collar employment represents a substantial share of discretionary spending.

The top income deciles account for a disproportionate share of housing, travel and durable goods demand.

Even modest declines in high-income employment could therefore have outsized macroeconomic effects.

Bond markets in the scenario begin pricing weaker consumption before equities fully adjust.

Private credit under strain

A key pressure point emerges in private credit, which expanded from under US$1 trillion in 2015 to more than US$2.5 trillion by 2026, according to the report.

Many leveraged buyouts of software firms were underwritten on assumptions of steady recurring revenue growth.

The firm highlights the case of Zendesk, taken private in 2022. In the scenario, AI-driven automation reduces demand for ticket-based customer support, leading to covenant breaches and sharp debt markdowns by 2027.

Downgrades by ratings agencies accelerate recognition of losses, challenging assumptions that private credit structures can absorb stress gradually.

Insurance linkages and market reaction

Alternative asset managers’ ownership of life insurers is identified as another transmission channel.

Groups such as Apollo Global Management, KKR and Brookfield have expanded into annuity businesses that allocate capital to private credit.

Rising defaults prompt tighter capital requirements, forcing asset sales or equity issuance in stressed markets.

In the scenario’s later stages, equity indices fall sharply as investors reassess correlated exposure to white-collar income stability.

Housing and mortgage stress

Housing becomes a focal point as employment declines in technology-heavy metropolitan areas.

The report references falling home values in cities such as San Francisco, Seattle and Austin, alongside rising delinquencies in high-income postcodes.

Unlike the 2008 crisis, borrowers initially possess strong credit scores and documentation. However, the underlying assumption of stable long-term income is challenged.

“The $13 trillion U.S. mortgage market rests on one core assumption: borrowers will remain employed at similar income levels for 30 years,” the report states.

Limits of traditional policy tools

Citrini Research argues conventional policy responses, including rate cuts and stimulus, may prove insufficient.

“It’s driven by AI making human intelligence less scarce and less valuable,” the authors wrote, describing a “collapse of the human intelligence premium”.

Proposals discussed include direct transfers to households, taxes on AI compute and public claims on AI-generated revenues.

However, the report warns political divisions could delay action.

“The real villain is time,” the analysts noted, adding that while the scenario is not inevitable, it highlights risks that merit preparation.

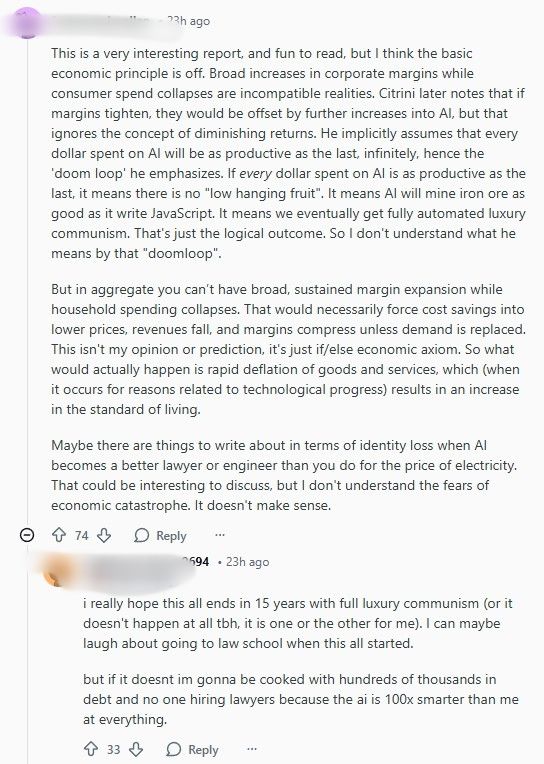

Economic assumptions challenged online

Online reactions to Citrini Research’s scenario were sharply divided.

Some readers argued the report misapplies core economic principles, particularly the claim that corporate margins could expand sustainably while household consumption contracts.

Several commenters contended that rapid technological deflation and rising consumer surplus would counterbalance disruption. Others emphasised that fiscal stimulus and monetary easing remain available tools to stabilise demand in the event of a downturn.

Fears over jobs and inequality

A number of participants voiced concern about white-collar job displacement, rising student debt burdens and downward social mobility.

Some warned of a future in which control over production, information and capital becomes concentrated among a small group of AI owners.

These commenters also raised the prospect of widening inequality, regulatory capture and the use of advanced surveillance or automation to suppress dissent if economic power becomes heavily centralised.

Another group rejected the idea that AI development would inevitably lead to monopoly control. They pointed to intensifying competition among major AI firms and the emergence of open-weight models, arguing that rivalry would constrain pricing power.

Some also questioned whether sectors such as healthcare and housing would be as vulnerable to rapid disruption as software, citing regulatory barriers and entrenched industry structures.

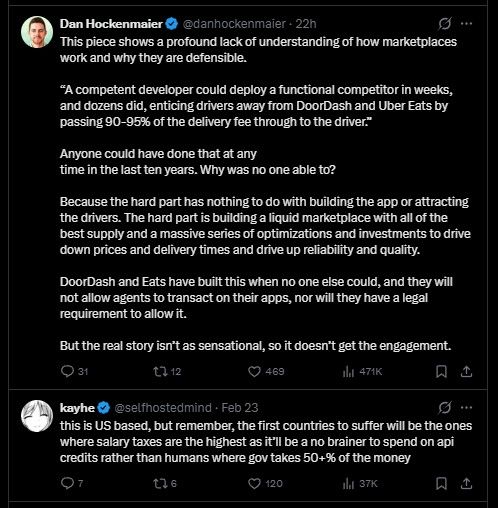

Questions about pace and platform defensibility

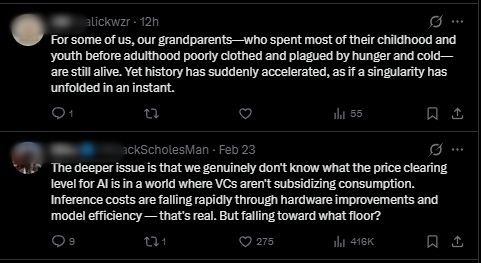

Several commenters expressed scepticism about the speed of AI transformation, noting that real-world workplace adoption remains inconsistent and, in some cases, underwhelming.

Others disputed the article’s claims about the fragility of digital platforms, arguing that delivery and marketplace businesses are defended not merely by software, but by complex network effects, scale advantages and operational optimisation that are difficult to replicate.