Jamus Lim renews call for Medisave flexibility through carry-over and age-based withdrawal limits

WP MP Jamus Lim has renewed calls to reform Medisave withdrawal limits, proposing a three-year carry-over system and age-based tiers to better reflect uneven healthcare costs and reduce out-of-pocket burdens.

- Jamus Lim proposes Medisave reforms to address uneven healthcare spending patterns.

- Suggested changes include three-year carry-over limits and age-based withdrawal tiers.

- Government says proposals are under review but stresses existing safeguards.

SINGAPORE: Workers’ Party Member of Parliament Associate Professor Jamus Lim has reiterated calls for reforms to Medisave withdrawal limits, arguing that existing rules do not reflect how individuals typically incur healthcare expenses.

In a Facebook post dated 14 April 2026, Lim revisited proposals first raised during the Ministry of Health’s Committee of Supply debate on 4 March.

He said the structure of Medisave caps fails to align with the “lumpy” nature of medical spending.

Lim framed the issue as a mismatch between predictable policy design and unpredictable real-world healthcare needs, where long periods of minimal spending are interrupted by sudden, high-cost episodes.

Lim described healthcare expenditure as inherently uneven, noting that most individuals incur little or no medical costs in many years, before facing significant expenses during major illnesses or procedures.

“We fall sick on occasion. But unless you’re the chronically ill type, you probably only visit your doctor only a couple of times a year,” he said.

“There may even be whole years where [you] don’t end up at the clinic at all. Yet when we do visit, it could well be something big.”

He cited examples such as accidents involving broken bones or serious diagnoses requiring surgery, where costs can rise sharply within a short period.

“That’s the nature of medical spending: we often don’t need it, but when we do, it may be big,” Lim added.

End-of-life costs drive spending patterns

Lim also highlighted research showing that healthcare expenditure is heavily concentrated towards the end of life, reinforcing the uneven distribution of medical costs.

“Health economists have long recognised that medical needs are lumpy. Expenditures are especially lumpy at the end of life,” he said.

“In fact, the evidence suggests that folks spend the most in the final months of their lives.”

He noted that such spending often involves intensive or invasive procedures aimed at prolonging life, contributing to a significant spike in healthcare costs during later years.

These observations, he said, underpin the rationale behind Medisave withdrawal caps, which are designed to preserve savings for future needs.

Limits designed for prudence

Medisave currently imposes annual withdrawal caps for both chronic conditions and major procedures.

The system is intended to prevent individuals from exhausting their healthcare savings prematurely.

Lim acknowledged that this principle remains sound.

“So it makes sense to preserve a chunk of our medical savings for end-of-life treatment,” he said.

“This is the premise for Medisave spending caps: you don’t want to blow all your savings early on, only to find yourself in a deep financial hole later.”

However, he argued that the system places too much emphasis on long-term preservation at the expense of flexibility in the present.

“There’s no point in preserving all your medical savings for that big whammy near the end, only to live in relative misery in the meantime,” he added.

Mismatch between caps and real costs

Lim said the current structure of flat annual caps does not adequately account for sudden spikes in medical expenses.

When individuals exceed these caps during a year with high healthcare needs, they are required to pay the remainder out of pocket.

For retirees, he noted, this often shifts the financial burden to their working-age children.

He also pointed out that the system does not fully account for the role of MediShield Life and other insurance schemes, which already cover major illnesses.

As a result, he suggested that concerns about depleting Medisave balances may be overstated.

Data suggests excess savings

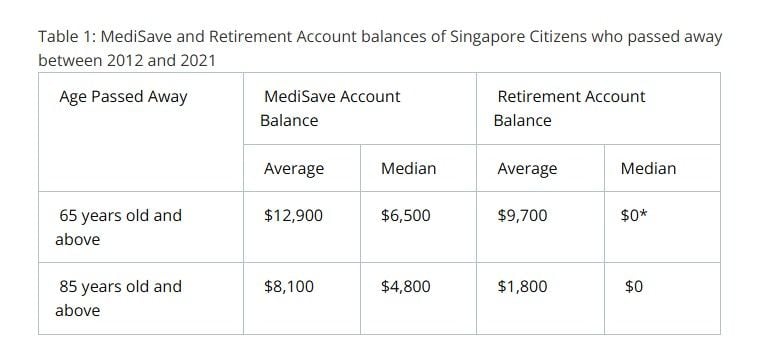

Lim cited Central Provident Fund data indicating that Medisave balances may be disproportionately large relative to retirement savings.

In a 2022 parliamentary reply, the Manpower Minister revealed that members aged 85 and above who passed away between 2012 and 2021, held Medisave balances nearly five times larger than their retirement account balances.

*A majority of the members in this group passed away after the age of 80 and may have fully utilised their Retirement Account monies by then. Older cohorts also tend to have lower RA balances due to more liberal withdrawal rules at age 55.

“This suggests there may be excess forced saving,” Lim said, adding that individuals could be contributing more to Medisave than they are able to utilise.

He argued that this imbalance supports the case for greater flexibility in how funds can be accessed.

Proposed reforms to improve flexibility

Lim proposed two policy changes aimed at aligning Medisave rules more closely with real-world healthcare needs.

The first involves allowing unused annual withdrawal limits to be carried forward for up to three years.

“If you don’t use your full withdrawal limit this year, you can ‘bank’ it for future years,” he said.

This would enable individuals to draw on accumulated limits during years of high medical expenditure, reducing the need for out-of-pocket payments.

The second proposal calls for a tiered system of withdrawal limits that increase with age.

Lim argued that since healthcare costs tend to rise as individuals grow older, withdrawal caps should reflect this progression.

“The second idea is based on how our spending needs… tends to rise with age,” he said.

He suggested that mortality statistics could be used to calibrate age-based limits.

Balancing flexibility and sustainability

Lim emphasised that both proposals are intended to preserve the underlying objectives of Medisave while improving access to funds.

“The principle behind these suggestions are simple: to improve flexibility in medical spending, as much as possible, while preserving the… motivation behind the need for spending caps,” he said.

He expressed hope that such refinements would better align policy with lived realities and reduce the accumulation of unused savings.

Health Minister earlier signalled openness to reviewing MediSave withdrawal flexibility

Health Minister Ong Ye Kung responded to Lim’s proposals on 5 March, acknowledging that the characterisation of healthcare spending patterns was accurate.

“Even after accounting for inflation, the average Singaporean living up to their mid-eighties spends almost four times as much on hospital expenses in the last ten years of their life, compared to the previous ten years,” Ong said.

He noted that this trend informs the current design of Medisave withdrawals, which prioritises preserving funds for later-life healthcare needs.

Existing flexibility measures

Ong highlighted that existing schemes already provide a degree of flexibility for everyday medical expenses.

These include Flexi-MediSave and MediSave500 or MediSave700, which allow withdrawals for chronic disease management, diagnostic tests and outpatient services.

“These schemes provide flexibility without overly diluting MediSave’s original objective of catering for these big lumpy hospital bills,” he said.

He added that after subsidies, MediShield Life coverage and Medisave withdrawals, nine in ten Singaporeans pay less than S$500 out of pocket for subsidised inpatient bills.

Proposal under review

Lim subsequently sought clarification on whether a limited carry-over mechanism could strike a balance between immediate flexibility and long-term savings preservation.

Ong said the proposal would not be accepted or rejected outright at this stage.

“I think it is an interesting idea. As I say we review the scheme every year,” he said.

He added that the ministry would study how to introduce greater flexibility without undermining Medisave’s core objectives.